FIT FIRST: FRAMEWORK FOR FIT

This post highlights the trade-offs between structures, examples of where alignment worked and failed, my worries with current trends, and a practical decision tree you can use to achieve alignment.

Structure is not just a pretty package to enhance sales; it can make or break the future of your firm.

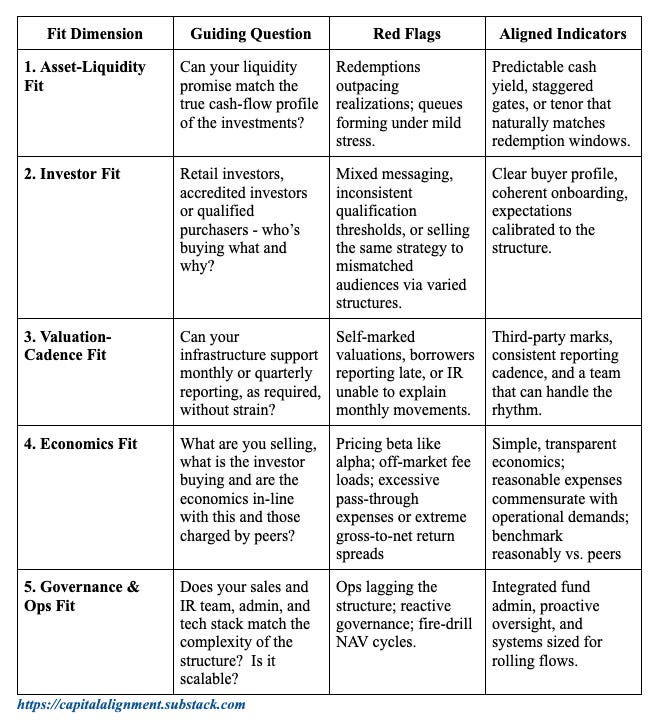

Think of this as your pre-launch alignment test. Structure only works when five kinds of fit hold: between your assets and your liquidity promise, your investors and their expectations, your valuation frequency and the quality of your reporting, your fees and your cash flows, and your governance and actual investor flows.

When any one of these fails, the fund may still raise capital, but it might fail on alignment.

Focus upfront on this Framework For Fit, but also come back to it as you scale.

1. Asset-Liquidity Fit: Can Your Assets Support the Liquidity You Promise?

Start with your investment approach: hold periods, realization patterns, dispersion, and the time horizon from investment to exit (both desired and realistic). Then compare that profile to the liquidity terms you want to promise.

If your value creation depends on multi-year compounding, concentrated positions, or event-driven exits, frequent liquidity creates structural tension. Interval and evergreen designs work when cash flows arrive steadily and predictably and investors behave independently. They break when investors panic and try to redeem with a herd-like mentality. Market forces outside of a manager’s control also create complications for these structures - like our current state of “stuck-ness.”

Redemption pressure tends to surface at the exact moment you prefer to lean in. If you find yourself drafting liquidity terms first and “figuring out the portfolio later,” stop. You need to start again with an investment strategy-first mindset.

2. Investor Fit: Do The Investors Understand What They’re Buying & Are You Delivering On What You Sold?

Institutions, QPs in 3(c)(7) vehicles, and retail-adjacent channels all approach liquidity and transparency differently. They also react differently under stress. A structure that appeals to an institutional allocator may seem completely foreign to a wealth-channel buyer.

The pressure to “go retail” can push managers to create structures that sell quickly but fit poorly. Take the example of a neighbor who told me he was so excited to be doing “AI” at work: “that’s where all of the growth is!” Confused, I asked how a bank back office was using Artificial Intelligence and what that had to do with growth. Alas, he was using their acronym for Alternative Investments. This particular bank wants all of its retail clients to hold 20% of their investments in alternatives.

I know how I feel about redeeming from a hedge fund investment in 2015 and not getting my money back until 2025 - TEN YEARS later! The decade long unwind did not generate returns sufficient to justify charging fees and holding my capital hostage. Plenty of LPs have horror stories from the GFC too when they tried to get liquidity and couldn’t.1

This year the Yale Model broke and caught sophisticated investors off guard - not sure anyone predicted forced selling of private equity by the likes of Yale and Harvard. Imagine what will happen when unsophisticated investors, new to the alternatives asset class, need liquidity and realize they’re stuck?

Ask yourself if your buyer-base can tolerate the journey your strategy requires? If not, changing the wrapper will not solve the problem. It will magnify it.

3. Valuation-Cadence Fit: Can Your Data and Your Investors Live in Harmony?

Monthly versus quarterly NAV drives an entire set of operational and behavioral dynamics. EY published a framework wholly dedicated to NAV reporting best practices that’s worth reviewing. Monthly cadence requires reliable borrower updates, credible third-party marks, and a valuation process sturdy enough to defend itself twelve times a year. It also creates more emotional touch points. More marks invite more interpretation. Sometimes accurate, often not.

In the face of increased market volatility I understand the temptation to “smooth” returns and avoid taking frequent marks but encourage you to ask yourself at what cost? What is the investor buying and are you delivering on what you sold? How does your cadence improve or impair the investor relationship?

The CastleRock experience detailed in the prior post illustrates an overlooked risk: transparency gives investors more information, but if not shared with appropriate context or misinterpreted, can reshape investor behavior.

A strategy can technically support more frequent marks yet still destabilize a franchise if existing investors did not sign up for or understand that level of visibility. A new wrapper can change how all investors experience your volatility, not just the investors inside that vehicle.

4. Economics Fit: Are The Fees & Expenses Reasonable vs. Competitors, What You Intend to Deliver & What Investors are Willing to Pay?

Managers often assume fees are a secondary consideration. Not so. Much like choosing a realtor, investors look closely at whether the fees they pay are justified by the value a manager provides.

Economics fit starts with a simple question: Are investors paying for alpha or beta? They will pay more for differentiated skill and less for general market exposure that they could buy more cheaply via other sources. Operational demands also matter. High-touch strategies, heavy data infrastructure, or complex execution can justify higher fees and expenses, just as a low-cost, rules-based approach should reflect its structural simplicity.

Premium returns can command premium fees. Brand, demand, and capacity constraints can tilt the equation too. Point72 charges up to 30% incentive fees versus an industry norm closer to 20%.

Uncorrelated returns can command excessive pass-through expenses. Multi-strats, in my opinion, have gone overboard with these. Hedgeweek has a good piece on this citing: “Bloomberg’s analysis shows that the list of eligible pass-through expenses among major multi-strats has grown by nearly 40% since 2018. While early disclosures focused on basic costs like rent and computers, today’s filings include items like artificial intelligence tools, severance payments, and even private jet bookings.” If you care about aligning investor interests with yours I suggest you evaluate each expense passed through versus the management fee you receive and try to find an appropriate balance. Looking at the gross-to-net return spread should help. Take Balyasny Atlas Enhanced for example: in 2023 the fund generated a gross return of 15.2%, although after fees, investors were left with just a 2.8% gain.

Retail-oriented structures often push distribution and shareholder servicing costs directly to investors, raising all-in expense ratios. Often they charge higher fees for accepting smaller minimums and offering better liquidity too. As more and more retail investors adopt alternatives thinking they are accessing higher, less correlated returns, what happens when net returns end up lower than traditional listed products?

Finally, remember that fees can misfire at the extremes. Price too high and you signal misalignment. Price too low and you undermine credibility. I know one manager who tried eliminating its management fee altogether as a good faith gesture to demonstrate alignment. Instead of attracting investors by only earning from performance, it deterred them; investors saw it as “off market,” perhaps interpreting it as desperate and walked. The lesson: economics must make sense relative to peers, costs, and what you deliver ultimately.

When the economics do not match the strategy or investor expectations, alignment breaks long before the portfolio gets a chance to work.

5. Governance & Ops Fit: Can Your Organization Actually Run the Structure You’re Selling?

Governance and operations determine whether a structure functions under real conditions. Evergreen, interval, and tender-offer vehicles require a higher level of board oversight, valuation documentation, liquidity management, and IR cadence than most managers anticipate.

Another overlooked risk: running “the same” strategy in multiple wrappers that drift apart in practice. Without discipline, weaker or longer-dated assets can quietly migrate into the vehicle with softer redemption pressure.

You also need to understand how investors intend to use your fund in their broader program: core allocation, tactical tilt, liquidity bridge. Their intended role drives the pattern of money moving in and out of the vehicle, which becomes an operational reality whether you plan for it or not.

If you map the vehicle at scale and something does not add up, stop there. That tension usually points to a structural issue worth addressing before you move forward.

When Structure Helps and When It Hurts

Fund structures can save or sink a firm. These three examples reveal the same truth: structure either reinforces your process or undermines it.

1. When Structural Aspects Protected Both the Firm and Investors (The Citadel Example)

In 2008, Citadel’s Kensington and Wellington funds experienced significant mark-to-market losses of roughly 55% during the market dislocation. Although the funds offered quarterly liquidity, they also had gates and the ability to suspend redemptions, tools designed precisely for periods of extreme stress.

While unpopular and very public, Citadel invoked those terms to avoid forced selling into a dysfunctional market. By gating redemptions, they stabilized the portfolios and unwound positions over time rather than liquidating at fire-sale prices. When redemptions resumed in 2009 and into 2010, performance had recovered materially. Investors who remained were able to participate in that rebound; investors who might have redeemed at the bottom avoided crystallizing losses.

Why it mattered: The liquidity structure reflected the strategy’s mix of liquid and less-liquid assets. In this case, disciplined alignment—rather than offering cosmetic liquidity—protected both the portfolio and the investor base.

2. When “Semi-Liquid” Promises Met Illiquid Reality (the BREIT Reminder)

Even Main Street knows about this one: a very public example of what happens when a structure sells better than it fits. BREIT offered periodic liquidity backed by inherently illiquid real estate. For years, strong inflows masked the mismatch. Then the market turned: rates rose, listed REITs sold off, and appraisal-based valuations didn’t adjust nearly as quickly as public markets.

Redemptions spiked. The fund hit its limits. Liquidity stopped being a feature and became a pressure point.

The structure did what it was designed to do when outflows outpaced what the underlying assets could provide. But investor expectations were very different. Many thought “periodic liquidity” meant “I can get out when I choose,” not “I can get out when conditions allow.”

Redemptions were gated first monthly, then quarterly. This caused frustration not only among the investors in the largest non-traded real estate investment trust in the U.S. but also for shareholders of the firm itself. Following the announcement, Blackstone’s (BX) stock fell by as much as 10% in a single day, its biggest drop since March of that year. The stock lost 43% of its value over the course of 2022 as a whole.

The takeaway: Semi-liquid structures only work when three things align:

The assets can support the liquidity,

The valuation process reflects real market conditions, and

The investors understand what the structure actually offers.

If any one of these falls short, the structure becomes the risk, not the solution.

3. When Liquidity Promises Broke the Vehicle (An Interval-Fund Fail)

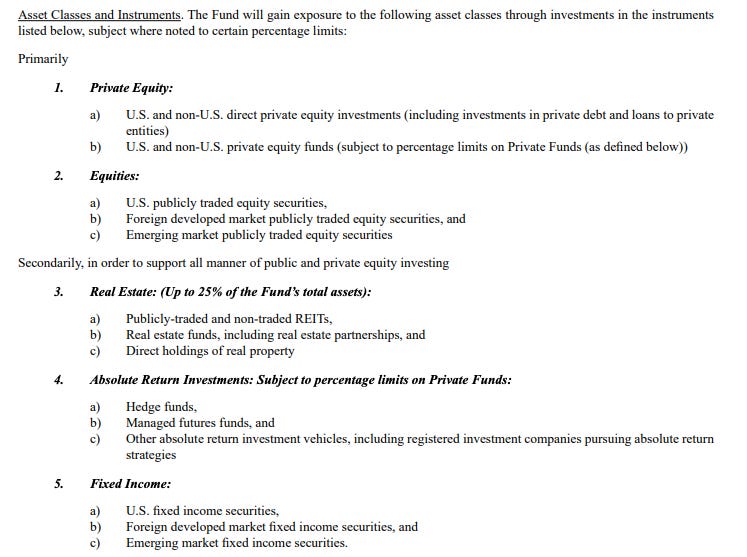

A clear real-world example of misalignment came from an interval fund that invested as follows (stated in the Prospectus):

The Adviser is responsible for the overall allocation of the Fund’s portfolio. The Adviser will seek to produce attractive risk-adjusted returns over time by investing in private investments that the Adviser believes to be of high quality supplemented by an allocation to liquid publicly traded equity investments. The Adviser invests in a mix of liquid, traditional equity and fixed income investments as well as less liquid, alternative and non-traditional investments.

Things that make ya go “huh?!?” I scratched my head when I learned about this “endowment model” portfolio being offered in an interval fund format with investment minimums of $2,500 ($1,000 for retirement accounts). Why wouldn’t you offer the traditional equity and fixed income investments in a listed open-end structure and the private equity, real estate and private funds investments in a longer-lock drawdown structure? Because you couldn’t sell privates to retail investors at such low minimums. Look what they put all in the same strategy and structure:

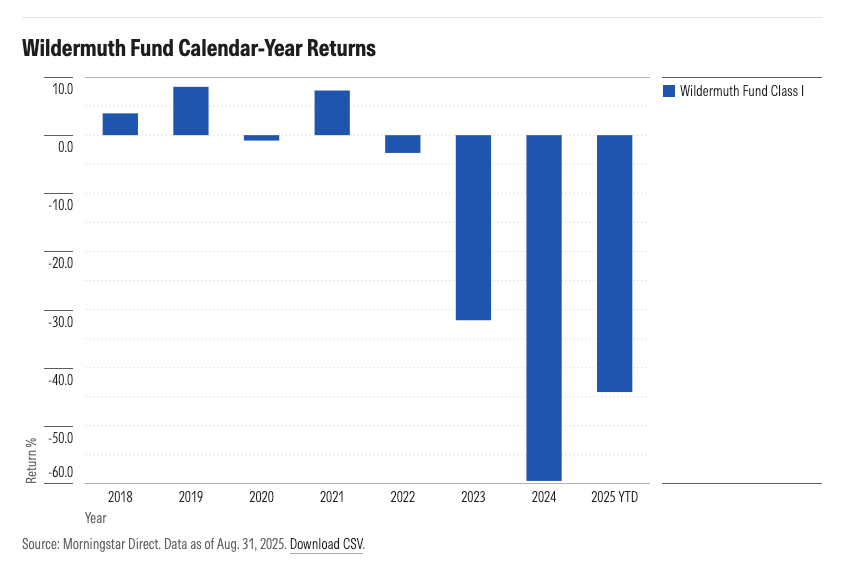

The following chart shows the evolution of returns starting after 2017 when redemption requests began en masse according to Morningstar. By 2020 the fund delayed its payout deadline after problems valuing some of its harder-to-sell investments caused an audit delay.

The cracks appeared. Redemptions accelerated. The fund couldn’t meet them. Transactions were suspended, and the vehicle entered a painful wind-down. The consequences were real: for investors and for the team running it. Structures do not fail quietly. They fail publicly.

The lesson: A structure that sells well is not necessarily the same as a structure that works. While the interval fund structure technically accommodated the holding of illiquid assets with liquid assets, the buyer base arguably was not well suited for this strategy. Poor performance compounded the issue. If your liquidity promise only holds when markets and investors behave perfectly, you do not have a liquidity feature, you have a structural liability.

Decision Tree / Checklist: The “Framework for Fit”

Before you land on a structure, run it through this framework. It only takes one flimsy fit to expose blow-up risk to your structure (and possibly firm).

If you can’t answer “yes” to at least four of the five, you don’t have product-market fit; you have product-market aspiration.

Final Thoughts: Structure Is Strategy

In fundraising, you can sell almost anything once. But structure determines whether you can manage it, scale it, and survive it.

A wrapper that looks clever in the short term can create long-term drag: the wrong investor base, too many unsophisticated clients demanding updates, or redemptions spiking at exactly the moment you want to double down on your best ideas. Misfit not only strains IR, but also it can change how you invest.

Product-market fit in fund design determines whether you scale or stall. Build a structure that reinforces your process, not one that erodes it.

If you’re designing a new vehicle or wondering why an existing one feels harder than it should, pressure-test the fit. Alignment compounds just like returns, but misalignment does too.

Like what you read? Remember to follow along and feel free to share:

Never miss a post: Subscribe to Capital Alignment on Substack for a deeper dive on fundraising realities, practical advice, and the human side of capital alignment.

Follow me on LinkedIn.

*That raises an entirely new consideration about investor fit. Your structure might be appropriate for your strategy and the investor aligned with both . . . but if the investor is overexposed to private investments, for example, and you’re running a quarterly liquidity hedge fund that has performed well, the investor might take profits from you to generate liquidity.

Disclosure & Disclaimer

All opinions expressed in this newsletter are strictly my own and do not represent the views of my firm, clients, or any affiliated broker-dealer. Nothing in this newsletter constitutes investment advice, a recommendation to buy, sell, or hold any security, or an offer to sell or a solicitation of an offer to buy any security. I am a registered representative of a broker-dealer. Readers should not act or rely on any information contained herein without first seeking independent professional advice from a qualified financial, legal, or tax advisor. Investing involves significant risk, including the potential loss of principal. Past performance is not indicative of future results. I may hold positions in, or have business relationships with, companies or securities discussed in this newsletter. Any material conflicts of interest will be disclosed when relevant, but readers should assume the possibility of a financial interest in topics covered. This newsletter contains only publicly available information and is not intended to disclose material non-public information. Certain statements herein may constitute forward-looking statements. Actual results, performance, or achievements may differ materially from those expressed or implied. While I strive for accuracy, I make no representations or warranties as to the completeness, accuracy, timeliness, or reliability of the information provided.